It’s a wonderful feeling when you can stop paying rent and start paying your own mortgage. Owning your own home is a dream that many people have, but not everyone will achieve. Owning your own home gives you greater financial freedom and is a great investment in your future. For most people, the process is very simple. You approach a lender and tell them about your earnings and how much deposit you can afford. If they agree to lend to you, you can start your house hunt and before long you’ll be moving into your own home. However, for the self-employed, the process looks very different.

With more people than ever before going down the self-employed route, it’s an issue that is going to arise with more frequency. So, here are the basic steps for getting a mortgage when you are self-employed.

In the past, the self-employed could use something known as the self-cert mortgage, but this has now been banned in the UK due to its widespread misuse. When individuals could simply state their own income without proof, some people used this to borrow more than they could afford. For this reason, self-cert mortgages were banned following the financial crash.

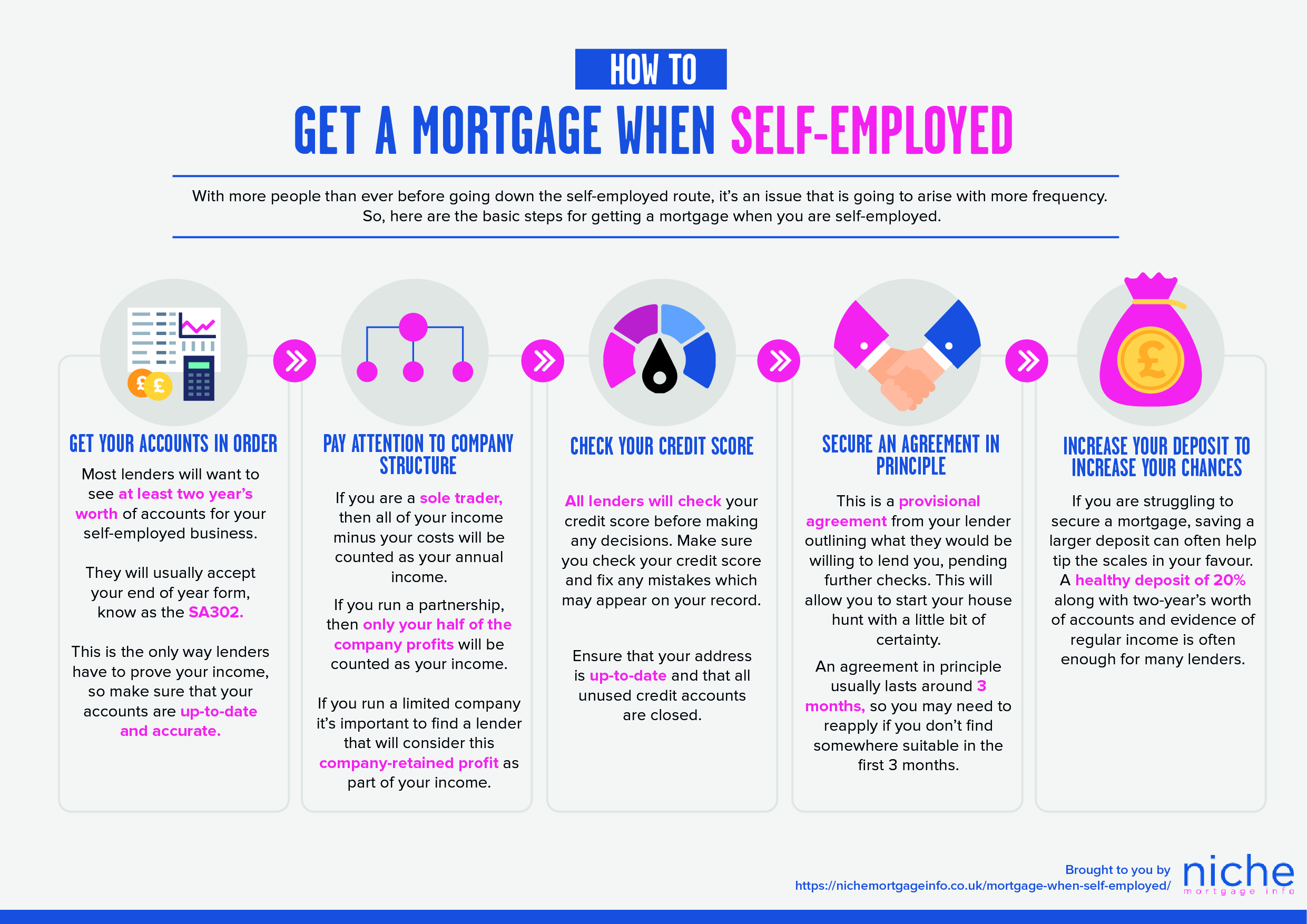

Most lenders will want to see at least two year’s worth of accounts for your self-employed business. They will usually accept your end of year form, know as the SA302. They might also want to see your accounts prepared by a registered and/or chartered accountant. This is the only way lenders have to prove your income, so make sure that your accounts are up-to-date and accurate.

It’s common for people to make legal adjustments to their income in order to lessen their tax liability, but this will work against you if you are trying to get a mortgage as it will appear that you earn less and lenders will, therefore, want to lend you less.

If you have more than 1 year of accounts, but less than 2, then lenders might be willing to make a projection based on the information they have or take the first full year’s income as the final amount. If you have more than one year’s worth of accounts and the numbers differ every year, the lender might take the most recent year as your annual income.

The way you have set up your company will have a huge impact on your mortgage possibilities. If you are a sole trader, then all of your income minus your costs will be counted as your annual income.

If you run a partnership, then only your half of the company profits will be counted as your income. And if you run a limited company and you leave money in the company at the end of the year, it’s important to find a lender that will consider this company-retained profit as part of your income. An accountant will be able to help you to structure your accounts in a way that is most attractive to lenders.

All lenders will check your credit score before making any decisions. Before you start applying for mortgages, make sure you check your credit score and fix any mistakes which may appear on your record. For example, you should ensure that your address is up-to-date and that all unused credit accounts are closed. If there are any mistakes on your record you can write to the creditor and request that they fix it and give you written confirmation that it is a mistake. Once you have a strong credit report, your application will look a lot more attractive to lenders.

If you are keen to start the house hunt but don’t want your mortgage application to delay the process then you can secure something known as an agreement in principle. This is a provisional agreement from your lender outlining what they would be willing to lend you, pending further checks. This will allow you to start your house hunt with a little bit of certainty. Once you have found a place you like, you can put in an offer, and if it’s accepted then you can put in your final mortgage application. An agreement in principle usually lasts around 3 months, so you may need to reapply if you don’t find somewhere suitable in the first 3 months.

If you are struggling to get accepted, don’t assume that no one will give you a mortgage. Some lenders are more experienced with self-employed individuals, so often it’s a case of finding the right lender or working with a niche mortgage broker. If you are struggling to secure a mortgage, saving a larger deposit can often help tip the scales in your favour. A healthy deposit of 20% along with two-year’s worth of accounts and evidence of regular income is often enough for many lenders.